Subrogation allows an insurer to recover the claim amount from the person or party responsible for the loss after settling the policyholder's claim. It applies to indemnity-based insurance, follows a defined recovery process, and determines when recovery rights can be exercised, the documents involved, and how it differs from indemnity, contribution, and assignment.

Your parked car is hit by another driver's vehicle, and your insurer settles the repair bill under your car insurance. A few months later, you learn that your insurer is recovering the same amount from the at-fault driver's insurer. If you've ever wondered how that works or whether you can also claim that money, you've already encountered the principle of subrogation. Here's what it means and why it matters in insurance.

What is Subrogation?

Subrogation is the legal transfer of one person's right to recover a loss to another after that loss has been compensated. The word comes from the Latin term subrogare, meaning "to substitute". Simply put, if someone pays for a loss caused by another person, they may acquire the legal right to recover that amount from the party responsible.

Suppose your friend clears a debt on your behalf because someone else failed to repay you. Your friend can then recover that amount from the original debtor. That transfer of recovery rights is known as subrogation.

What is Subrogation in Insurance?

Subrogation in insurance is the insurer's legal right to recover the claim amount from the third party responsible for the insured loss after settling a valid claim. After settling a valid claim, the insurer acquires the policyholder's legal right to recover the amount paid from the third party responsible for the loss.

This principle was explained by the Supreme Court of India in Economic Transport Organisation v. Charan Spinning Mills (2010). In this case, goods insured during transit were damaged, and the insurer compensated the policyholder under the insurance policy. The insurer then sought to recover the amount from the transporter alleged to have caused the loss. The Court clarified that, after settling a valid claim, an insurer acquires the insured's right to recover the loss from the responsible third party through subrogation.

Principle of Subrogation in Insurance

The principle of subrogation gives an insurer the legal right to "step into the shoes" of the policyholder after settling a valid claim. This allows the insurer to recover the claim amount from the third party responsible for the loss, ensuring the insured does not receive compensation twice for the same incident. It also reinforces the principle of indemnity by placing the financial burden on the party at fault.

Key Principles

- Transfer of recovery rights

Once the claim is paid, the insurer acquires the policyholder's right to recover the loss from the legally liable third party. - Supports the principle of indemnity

Insurance restores the insured to the financial position they were in before the loss. It is not meant to create a financial gain. - Prevents double recovery

The policyholder cannot recover compensation from both the insurer and the person responsible for the same loss. - Recovery is limited

The insurer can recover only up to the amount it has paid under the claim. If a higher amount is recovered, tIf the recovery exceeds the insurer's payout, the distribution of the excess depends on the policy terms and the applicable law. - Claim settlement comes first

The insurer's right of subrogation arises only after a valid claim has been settled under an indemnity-based insurance policy.

Quick Examples

- Motor Insurance

Another driver damages your parked car. Your insurer pays for the repairs under your comprehensive policy and later recovers the amount from the at-fault driver's insurer. The same goes for bike insurance. - Health Insurance

You are injured in a road accident caused by another person. Your health insurance settles your hospital bill first and may later recover the claim amount from the person responsible or their liability insurer. - Business Property Insurance

A neighbouring factory's negligence causes a fire that damages your warehouse and inventory. Your insurer compensates you for the covered loss and may subsequently recover the amount from the neighbouring business or its liability insurer if it is legally liable.

Doctrine of Subrogation in Insurance Law

The doctrine of subrogation is a long-established legal principle that originated in English common law and is based on the principle of indemnity. It authorises the insurer to exercise the insured's legal right of recovery against the party responsible for the loss.

In India, this doctrine forms part of the law governing indemnity-based insurance contracts and has been consistently recognised by Indian courts. It is also expressly recognised under Section 79 of the Marine Insurance Act, 1963, which grants insurers the right of subrogation in marine insurance after indemnifying the insured. The same equitable principle is applied across other indemnity-based insurance policies, including motor, property and indemnity-based health insurance, through judicial interpretation and established insurance law.

Legal Note: The doctrine of subrogation applies only to contracts of indemnity. It does not apply to benefit-based insurance products such as life insurance, critical illness insurance that pays a fixed lump sum, or hospital cash policies.

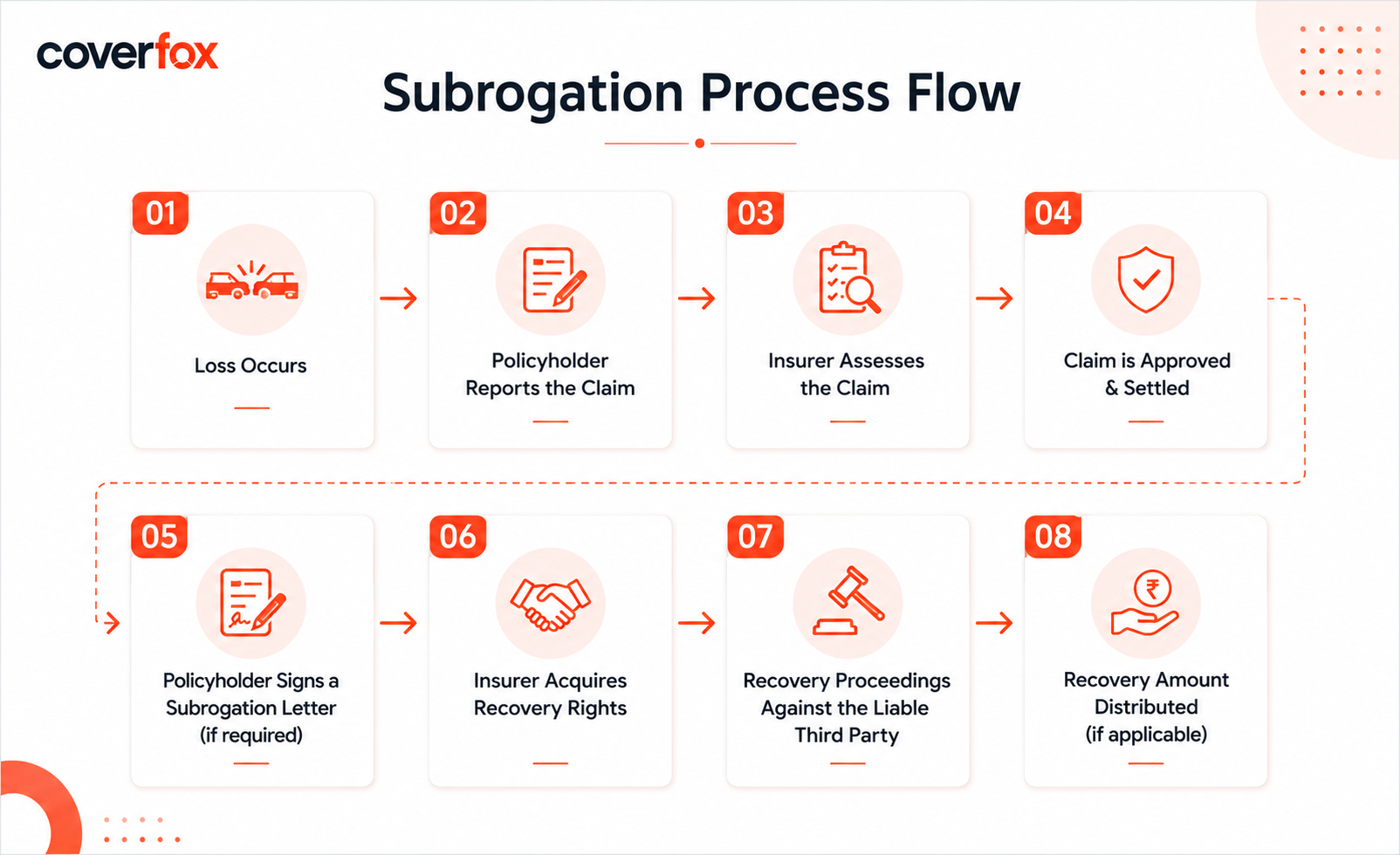

How Does Subrogation Work in Insurance?

Subrogation begins only after a covered loss occurs and the insurer settles the policyholder's claim. The insurer then initiates recovery proceedings against the third party responsible for the loss.

Subrogation Process Flow

Step 1: Loss Occurs

A covered loss occurs because of the actions or negligence of a third party. This could include a road accident, property damage, or injuries caused by another person.

Step 2: Policyholder Reports the Claim

The policyholder informs the insurer, submits the required documents, and provides details of how the incident occurred.

Step 3: Insurer Assesses the Claim

The insurer verifies whether the loss is covered under the policy, evaluates the extent of the damage, and determines whether a third party is legally liable.

Step 4: Claim is Settled

If the claim is approved, the insurer settles it according to the policy terms. Only after payment can recovery proceedings begin.

Step 5: Subrogation Letter or Agreement

Where required, the policyholder signs a subrogation letter or subrogation agreement, authorising the insurer to recover the claim amount from the responsible third party.

Step 6: Recovery Proceedings Begin

The insurer contacts the liable third party or their insurer to recover the amount paid. If the matter cannot be resolved through negotiation, the insurer may initiate legal proceedings.

Step 7: Recovery Amount is Distributed

The insurer retains the recovered amount up to the claim it has paid. If the recovery exceeds the insurer's payout, the remaining amount may be payable to the policyholder, depending on the policy terms and applicable law.

Note: The subrogation process takes place in the background after the claim has been settled. In most cases, the policyholder's involvement is limited to providing documents, preserving evidence, and cooperating with the insurer during the recovery process.

Types of Subrogation in Insurance

The right of subrogation can arise in different ways depending on the insurance contract and the legal basis for recovery. The three main types of subrogation are equitable, contractual and statutory.

1. Equitable Subrogation

Equitable subrogation is the most common form of subrogation. It arises automatically once the insurer indemnifies the policyholder for a covered loss. The insurer can then recover the amount paid from the third party responsible for causing the loss without requiring a separate contractual provision.

2. Contractual Subrogation

Contractual subrogation arises from the terms of the insurance policy or a separately executed subrogation agreement. The policyholder expressly authorises the insurer to pursue recovery from the liable third party after settling the claim. This type is commonly seen in motor, health and commercial insurance policies.

3. Statutory Subrogation

Statutory subrogation exists where legislation specifically grants the insurer the right to recover losses from a third party. In India, this right is expressly recognised under Section 79 of the Marine Insurance Act, 1963, which codifies the insurer's right of subrogation after indemnifying the insured under a marine insurance policy.

Note: Although statutory recognition exists under the Marine Insurance Act, the doctrine of subrogation is also recognised and applied to other indemnity-based insurance contracts, including motor, property and indemnity-based health insurance, through common law principles and contractual terms.

Subrogation Letter and Subrogation Agreement

Depending on the nature of the claim, the insurer may ask the policyholder to execute a subrogation letter or agreement before beginning recovery proceedings. These documents enable the insurer to recover the claim amount from the third party responsible for the loss after the claim has been settled.

Although the terms are often used interchangeably, they differ in scope and purpose.

| Aspect | Subrogation Letter | Subrogation Agreement |

|---|---|---|

| Meaning | A written authorisation allowing the insurer to recover the claim amount from the responsible third party. | A formal legal contract that defines the insurer's subrogation rights and the policyholder's obligations. |

| Purpose | Confirms the transfer of recovery rights after claim settlement. | Sets out the terms governing the insurer's right to pursue recovery. |

| When it is Signed | Usually after the insurer approves or settles the claim. | Signed when the insurer requires a detailed legal agreement as part of the claims process. |

| Legal Scope | Limited to authorising recovery of the amount paid. | Broader in scope and may include cooperation obligations, legal procedures and other recovery-related terms. |

| Common Usage | Frequently used in motor and property insurance claims. | More common in complex or high-value claims, commercial insurance and marine insurance. |

What is a Subrogation Letter?

A subrogation letter is a written declaration by the policyholder authorising the insurer to recover the claim amount from the third party responsible for the loss. It confirms that, after receiving claim payment, the policyholder transfers the right to pursue recovery to the insurer to the extent of the amount paid.

What is a Subrogation Agreement?

A subrogation agreement is a more comprehensive legal document that records the insurer's recovery rights and the policyholder's responsibilities during the recovery process. It may require the policyholder to provide documents, preserve evidence and cooperate with the insurer if legal proceedings become necessary.

Note: Signing a subrogation letter or agreement does not reduce the claim amount payable under the policy. It simply enables the insurer to recover the amount paid from the party legally responsible for the loss, where applicable.

Rights and Responsibilities During Subrogation

Once an insurer settles a valid claim, it may exercise its right of subrogation against the third party responsible for the loss. At the same time, the policyholder has certain responsibilities to ensure the recovery process is not affected.

Rights of the Insurer

After settling the claim, the insurer has the right to:

- Recover the claim amount from the third party legally responsible for the loss.

- Initiate negotiations or legal proceedings against the liable party, where necessary.

- Recover only up to the amount paid under the insurance policy.

- Seek the policyholder's cooperation by requesting documents or information required during the recovery process.

Responsibilities of the Policyholder

During the subrogation process, the policyholder is expected to:

- Cooperate with the insurer throughout the recovery process.

- Provide relevant documents, such as accident reports, medical records, repair estimates, invoices or other evidence supporting the claim.

- Preserve evidence related to the loss, wherever possible, until the insurer completes its assessment.

- Avoid settling with or releasing the responsible third party from liability without the insurer's consent, as doing so may affect the insurer's recovery rights.

- Sign a subrogation letter or subrogation agreement if required as part of the claims process.

Waiver of Subrogation Clause in Insurance Policy

A waiver of subrogation is a contractual provision under which the insurer agrees to give up its right to recover the claim amount from a third party responsible for the loss. As a result, even after settling a valid claim, the insurer cannot pursue legal action against the party covered by the waiver.

This clause is commonly used where two parties have an ongoing commercial relationship and want to avoid disputes or litigation after an insured loss.

Where is a Waiver of Subrogation Commonly Used?

A waiver of subrogation clause is frequently included in:

- Construction and infrastructure contracts

- Commercial lease agreements between landlords and tenants

- Business partnership and joint venture agreements

- Vendor and supplier contracts

- Large commercial property and engineering projects

Advantages of a Waiver of Subrogation

- Reduces the risk of legal disputes between contracting parties.

- Helps preserve long-term business relationships.

- Simplifies claim settlement by preventing recovery proceedings against the other party.

- Provides greater contractual certainty in projects involving multiple stakeholders.

Disadvantages of a Waiver of Subrogation

- The insurer loses its right to recover the claim amount from the party responsible for the loss.

- Some insurers may charge a higher premium before agreeing to include a waiver of subrogation endorsement.

- The waiver may not apply unless it is specifically endorsed or permitted under the insurance policy.

- It can increase the insurer's financial exposure, as the loss cannot be recovered from the negligent party.

Difference Between Subrogation, Indemnity, Contribution, & Assignment

| Basis | Subrogation | Indemnity | Contribution | Assignment |

|---|---|---|---|---|

| Meaning | The insurer acquires the insured's right to recover the claim amount from the third party responsible for the loss. | The insurer compensates the insured for the actual financial loss suffered. | Two or more insurers share the claim liability when the same risk is insured under multiple policies. | The insured transfers their legal rights or interest in a policy or claim to another person or entity. |

| Purpose | To recover the claim amount from the party at fault and prevent double compensation. | To restore the insured to the financial position they were in before the loss. | To ensure each insurer pays only its fair share of the claim. | To transfer ownership of rights or benefits from one party to another. |

| Transfer of Rights | Recovery rights transfer to the insurer after claim settlement. | No transfer of rights takes place. | No transfer of rights takes place. | Rights are transferred to the assignee as per the assignment. |

| Who Can Exercise It? | The insurer after settling a valid claim. | The policyholder by making a valid claim. | All insurers cover the same insured risk. | The assignee who receives the assigned rights. |

| Applicability | Indemnity-based insurance such as motor, property, fire and indemnity-based health insurance. | All indemnity-based insurance contracts. | When multiple insurance policies cover the same subject matter and risk. | Where the policy or law permits assignment, such as life insurance or transfer of policy rights. |

| When It Applies | After the insurer has settled the claim. | At the time of claim settlement. | When more than one insurer is liable for the same loss. | When the assignment is executed according to the policy terms and applicable law. |

| Recovery/Compensation Limit | Limited to the amount paid by the insurer. | Limited to the actual financial loss suffered. | Each insurer contributes proportionately to the loss. | Depends on the rights transferred under the assignment. |

In Simple Terms

- Indemnity ensures you are compensated for your actual financial loss.

- Subrogation allows the insurer to recover that compensation from the party responsible for the loss.

- Contribution comes into play when more than one insurer covers the same risk, ensuring each insurer pays only its proportionate share.

- Assignment transfers ownership of policy rights or benefits from one party to another, unlike subrogation, where only the right to recover is transferred.

Why is Subrogation Important in Insurance?

Subrogation ensures that insurance remains fair for everyone involved. It prevents policyholders from receiving double compensation, holds the party responsible for the loss financially accountable, and allows insurers to recover claim payouts from negligent third parties. By allowing insurers to recover valid claim payouts, subrogation also helps keep insurance premiums more sustainable over time.

FAQs on Subrogation in Insurance

What is subrogation in simple words?

Subrogation is the insurer's legal right to recover the claim amount from the third party responsible for the loss after settling a valid insurance claim.

Is subrogation applicable to life insurance?

No. Subrogation does not apply to life insurance because it is a benefit-based policy and not a contract of indemnity.

Does subrogation apply to health insurance claims?

Yes, but only to indemnity-based health insurance policies where a third party is legally responsible for the insured's injury or medical expenses. It does not apply to fixed-benefit covers such as critical illness or hospital cash policies.

Does subrogation apply to motor insurance claims?

Yes. If another person is responsible for damaging your insured vehicle, your insurer may recover the claim amount from the at-fault party or their insurer after settling your claim.

Can a policyholder refuse to sign a subrogation letter?

A policyholder may refuse, but doing so can affect the insurer's ability to recover the claim amount. If the policy requires execution of a subrogation document as part of the claims process, refusal may have implications under the policy terms.

What happens if the third party refuses to compensate the insurer?

The insurer may negotiate with the third party or initiate legal proceedings to recover the claim amount. The outcome depends on the available evidence and the applicable law.

Can an insurer recover more than the amount paid under subrogation?

No. The insurer's recovery is limited to the amount it paid under the insurance claim.

Who receives the money recovered through subrogation?

The insurer retains the recovered amount up to the value of the claim it paid. If any excess amount is recovered, its distribution depends on the policy terms and the applicable law.

Can subrogation happen without the policyholder's consent?

Yes. The insurer's right of subrogation arises once it settles a valid claim under an indemnity-based policy. However, insurers may still ask the policyholder to sign a subrogation letter or agreement to facilitate recovery from the third party.

How long does the subrogation process take?

There is no fixed timeline. The duration depends on factors such as the complexity of the case, availability of evidence, negotiations between insurers, and whether legal proceedings are required.

Does subrogation affect the No Claim Bonus (NCB) in motor insurance?

Not necessarily. The impact on your No Claim Bonus depends on the insurer's underwriting guidelines, the circumstances of the claim, and whether the claim is ultimately recovered through subrogation. Always check your policy terms.

Is subrogation mandatory in every general insurance policy?

No. Subrogation applies to indemnity-based insurance contracts where a third party is legally responsible for the loss. Its application depends on the nature of the policy and the circumstances of the claim.

Which law governs subrogation in India?

Subrogation is recognised under Indian common law as part of the principle of indemnity. It is expressly codified for marine insurance under Section 79 of the Marine Insurance Act, 1963, and is recognised by Indian courts for other indemnity-based insurance contracts.

Can a policyholder directly sue the third party after subrogation?

After the insurer has exercised its subrogation rights, the insurer is entitled to recover the amount it paid from the responsible third party. The policyholder may still pursue any uninsured or unrecovered portion of the loss, subject to the policy terms and applicable law.