With the innovation in the insurance segment, at times, more than one option is available. Riders like Personal Accident or a Critical Illness is available with life insurance policy as well as a stand-alone policy. Here’s how you can make your mind to cherry-pick the most apposite one.

Riddhima was confused. She was buying a life insurance term plan online for herself and as she was completing the process, she was presented with an option to buy riders for personal accident and critical illness at a nominal premium. At first impulse, the premium for riders seemed cheap however she thought to pause and think whether it is worthwhile to add a rider or purchase a standalone accident or a critical illness policy.

Riddhima is not alone in this confusion. It always happens that individuals who want to purchase insurance face with this dilemma. In this article, let us explore the pros and cons of the issue and help you decide which option is best suited for you. Meaning of standalone health insurance policy vs. rider in life insurance

In India, you can purchase a life insurance policy from a life insurance company whereby apart from covering you for death risk, the policy can also offer you a rider cover for accident, critical illness, waiver of premium etc. Not all life insurance policies offer all riders so it depends from policy to policy. As per IRDAI (Protection of Policyholders Interests) Regulations, 2002, the premium for rider cannot exceed 30% of the premium for the base product. The terms and conditions for rider coverage are spelled out in the policy terms and conditions. Here, in one policy, you are covered for death as well as accident & critical illness. So, that is one option for you.

Another option is to purchase a standalone policy for accident or critical illness. In such a case, your life insurance policy will only cover you for death risk. In case of accident or critical illness related claim, you’ll have to claim from the separate standalone policies. So, here you have 2 or 3 policies.

Comparison between standalone health policies vs. rider in life insurance

Now, let us come to the big question: whether you should purchase a standalone health policy vis a vis a rider in a life insurance policy. For doing that, let us compare both options on various parameters as follows:

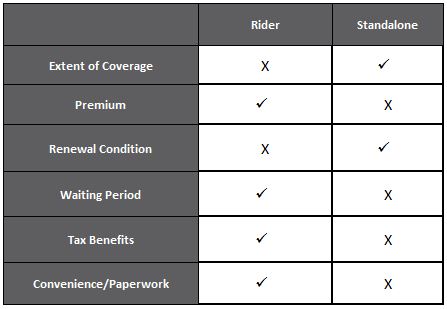

1. Extent of coverage:

When you purchase insurance, first thing you need to look at is getting the widest possible coverage at a decent price. So, the first thing you need to do is to compare the coverage available in an accident or a critical illness rider in a life insurance policy vis a vis the coverage available in a standalone policy. Generally, a standalone policy offers far more comprehensive coverage as compared to a rider. For e.g. Apollo Munich’s IPA Exclusive plan is one of the few comprehensive standalone policies that cover fractures and broken bones. In case of critical illness, you can check the number of illnesses that are covered in both options.

One reason why riders are not comprehensive is because it will increase the cost. Here, the IRDAI (Protection of Policyholder Interests) Regulations, 2002 specifically mandate that the premium relatable to rider for accident and critical illness cannot be more than 100% of the premium for base product. Also, rider benefit cannot exceed sum assured under the basic product. So, if your requirement for life insurance is Rs. 50 lacs & for disability is Rs. 1 crore, under the present regulations, you will not be able to get a disability cover for more than Rs. 50 lacs, which may prove to be inadequate.

2. Premium:

Premium in case of standalone policy is most likely to be higher considering the better coverage that is available as compared to a rider in case of a life insurance policy. Also, in case of a standalone policy, premium will increase basis your age group whereas in case of rider, it will remain constant throughout the term of your policy.

3. Renewal condition:

Standalone accident or critical illness policies come within the purview of IRDAI’s Health Insurance Regulations, 2013, which mean that these policies once issued, are renewable for life. As against this, a rider will be active only till the policy term of the base life insurance policy. So, to understand this with the help of an example: if you are 30 years old & purchase a life insurance policy with a policy term of 30 years, the policy (along with the attached riders) will cease at your age of 60. However, if you require cover for critical illness/disability at that point, it will be very difficult to purchase a standalone policy at that point in time. Against this, if you’ve purchased a standalone policy and continue to renew it without a break, insurer cannot deny renewal to you in your lifetime.

4. Waiting period condition:

In case of rider in a life insurance policy, accident and critical illness get covered from day one and generally there is no waiting period. However, in case of standalone policies, there is a waiting period clause of 30 to 90 days.

Also Read: The know-hows of Waiting Periods in Health Insurance

5. Tax benefits:

Tax benefits are available on premium paid for riders under Section 80C/80D of the Income Tax Act, as applicable. In case of standalone policies, whereas Section 80D benefit is available for mediclaim and critical illness policies, there is no tax benefit in case of accident policies. Hence, from an accident insurance perspective, a rider purchased along with a life insurance policy offers a tax advantage vis a vis a standalone accident policy.

Also Read: 'Must-Know' Differences between Tax-Deductions on Life and Health Insurance Premiums

6. Documentation and paperwork:

Accident and critical insurance rider purchased along with a life insurance policy effectively makes your life insurance policy a three-in-one policy thereby helping you create a compact insurance portfolio. So, neither do you need not maintain separate policy documents for each policy nor need to remember separate policy renewal dates etc. In case of standalone policies, it will be a bit more effort in terms of managing multiple policies.

Here’s the summary of the above:

Coverfox Verdict:

Above we’ve discussed the pros and cons of both standalone policy and riders. Before choosing which option is better, Riddhima should first check her requirements. If the primary consideration is to purchase a policy with a better coverage on all parameters (never mind a bit more premium and effort in managing multiple policies), standalone policy is her answer. However, if she is ok with lesser features and coverage, but stress more on the convenience aspect, then a rider will do the job for her. Either ways, one must read the policy wordings thoroughly to understand the policy features before exercising any specific option.

Recomended Read: Life Insurance or Health Insurance! Which one you should Opt for?