Basically there are 3 ways in which you can handle your planned and unplanned health care expenses:

(Photo Credits: Sturant Pilbrow)

Most of us can afford to pay for the treatment of minor medical problems ourselves, but are scared of the huge medical bills that come with serious diseases. Did you know that there are health insurance plans in India that are tailor-made for such situations?

So now the question is how to plan your health Insurance coverage such that it is cost effective and cheaper.

Basically there are 3 ways in which you can handle your planned and unplanned health care expenses:

1. TAP into your savings: Not recommended at all. For minor ailments – maybe yes, but definitely breaking the bank for heavier expenses is not the smartest way to go about it.

2. Group Health cover by employees: If you’re working at an organization, which offers health insurance coverage for employees, that’s awesome. As there is some protection there. But mostly it’s never enough. Employer provided health insurance in India, can be quite restrictive. And it’s not in your control.

3. Get yourself a health insurance cover: This would be the most feasible option of the three. Complete control on your healthcare. That’s what we are looking for, aren’t we?

The question is – how do I get cheaper health Insurance coverage if already have some health coverage from my employer or can manage to pay up to a certain limit (say Rs. 1-2 Lacs) in case of a health scare.

So here is a secret, a hidden gem - on how to save upto 40% on your Health Insurance. Read on…

TOP UP PLANS:

If you have a car, you would know the risk of driving without a spare tyre. A top up health cover works on the similar principle playing the similar role as that of a stepney to your base insurance (your own or offered by your employer) after you exhaust the sum insured limit.

A regular policy usually reimburses hospital bills up to the sum insured while on the other hand a health insurance top up plan covers costs after a certain threshold is reached.

Such policies are much cheaper than normal policies.

You pay the first one or two lakhs yourself (called the threshold limit or deductible) and if the hospital bill exceeds, then the insurance company pays the rest.

NOTE: You could bust the limit on your base health insurance for 2 reasons -

Your actual expenses were higher than your allowed cover or sum assured. Implying that if you had a higher cover, it would get paid. In this case a top-up pays for the balance

You underwent treatments which your base health insurance does not allow. OR you went to a premium very expensive hospital and your policy had some limits on how premium can you go – In this case your top-up will not help.

Top-ups work like your base policy. If something is restricted in your base, it will also be restricted in your top-up. So, it doesn't offer more benefits –it offers a higher limit on the same benefits. Specific restrictions remain the same.

TOP UP Vs REGULAR HEALTH INSURANCE COVER:

A top-up health insurance covers once the “threshold” limit is already used.

Let’s take an example. Assume that one has top up health cover plan of Rs 10 lacs sum assured with the threshold limit of 5 lacs, in this case the policy will cover expenses beyond Rs 5 lacs only.

Tip: The difference between normal mediclaim and top up plan is the deductible amount. Policy holder has to opt for deductible amount (shown as the threshold) at the time of buying the fresh plan.

Also, in the top up policies, most insurers do not ask for medical check-ups up to the age of 55 years. In basic plans, this is usually 45 years.

You need to buy a top up plan to bridge the gap between existing policies and actual costs. Your actual cover could be low and you need to adjust it to meet rising health care expense. That’s when a top-up works the best.

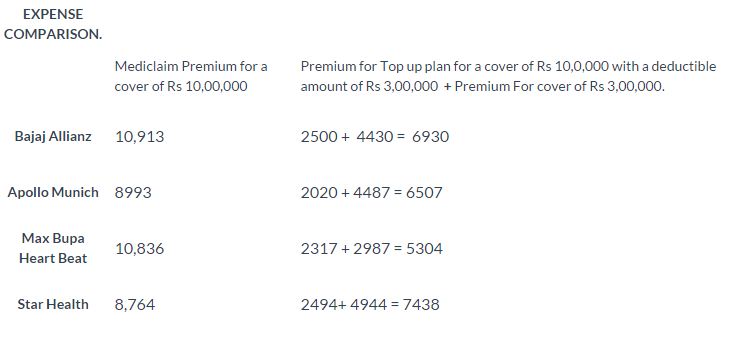

How cheap is a top-up health insurance cover?

Now, why wouldn't you simply raise the sum assured on your base plan? Because that would cost you around 40% more and our whole idea is to make your health insurance coverage cheaper.

Ok, let us see how can you save your hard earned money?

See the difference? You could save up to 40% !

Quickly now, a bit on TYPES OF TOP UPS, so you get it just right

Basic Top-up:

With a basic plan, the cover kicks in only when the deductible amount is exhausted within a single hospital visit.

Let’s check it out with an example -

5 Lac basic health insurance – 10 Lac top-up with 5 Lac threshold or deductible.

In the same year if you incur expenses twice due to hospitalization

1st time – Rs.3 Lacs

2nd Time – Rs. 4 Lacs

You have bust your cover. In a year you have spent 7 lacs on a basic health insurance of Rs. 5 lacs. But the balance 2 Lacs won’t be paid by the top-up plan.

Why? - you have to bust your limit in one instance of hospitalization - one visit, not in a year.

Is there a better option?

Super top up plan

A Super top cover on the other hand will consider TOTAL amount of bills in a year not just for a single instance. So in the above example, a super top-up would be a better product.

A LITTLE MORE TO KNOW

Now that you know about top up plans and super top up plans, here are some top-up plans available via leading Health Insurance Companies with their coverage amount and deductible.

WHILE BUYING A TOP UP PLAN

Consider the exact requirement for self or for the family.

The top-up plan's deductible should be less than or equal to the base policy sum insured.

Top-up plans provide dual benefits of low cost and higher sum insured.

For all those who have parents about to enter the senior citizen category, this would be the perfect product. As that is the time when the probability of falling ill is high and medical expenses are bound to increase.

For the salaried, who are covered under employer’s health insurance policy should also buy a top-up plan for higher protection.

Top-ups are one of the cheapest and best ways to enhance your coverage, without shelling out a lot of money. Build them into your healthcare planning. It’s simple, cheaper and effective.

Recommended Link: What is Health Insurance? How to Decide the Coverage Required?</b>