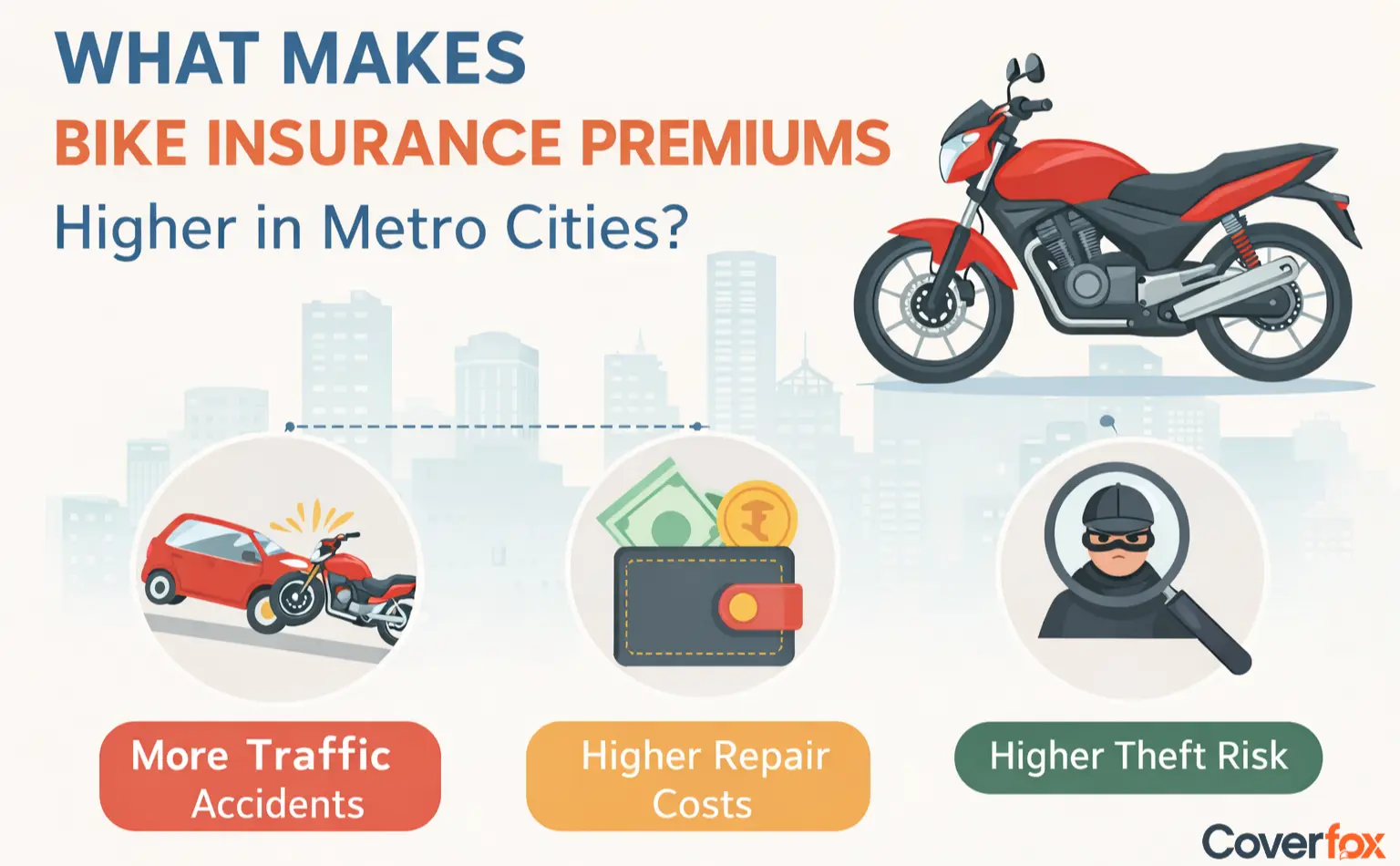

Bike insurance premiums are generally higher in metro cities (Zone A) because insurers consider these locations riskier due to higher accident rates, theft incidents, traffic congestion, and repair costs. Insurers use a zone-based pricing system where major metro cities fall under Zone A, while most other cities and towns are classified as Zone B, which usually has lower premiums. Even in metro cities, riders can reduce premiums through No Claim Bonus (NCB), anti-theft devices, higher deductibles, and careful selection of add-ons.

Living in a city is far more expensive than living in a rural area. There are many factors that influence this discrepancy, like the standard of living, the cost of consumer goods, population, infrastructure, etc. Similarly, bike insurance in metro cities can be more expensive than in other rural/urban centres. This article will showcase why the difference between the premiums.

How Location Impacts Bike Insurance Premiums?

Bike insurance premiums are generally higher in metro cities because insurers classify these locations as high-risk zones (Zone A). Metro areas usually have higher accident rates, more vehicle theft cases, expensive repair costs, and heavier traffic, all of which increase the likelihood of claims. Because of this higher risk exposure, insurers charge a higher premium for bikes registered in major cities.

Bike insurance prices are not fixed across India and vary depending on the city where the bike is registered. Insurers analyse city-wise risk data such as accident frequency, theft statistics, and repair expenses to determine premium pricing. As a result, bikes registered in metro cities typically attract higher premiums compared to those registered in smaller towns or rural areas.

Zone-Based Pricing in Bike Insurance

Insurance companies in India use a zone-based pricing system to calculate bike insurance premiums. Cities are broadly divided into Zone A (metro and high-risk cities) and Zone B (other cities and towns) based on historical risk data such as accident frequency, theft rates, traffic density, and repair costs. Since the risk of claims is higher in metro areas, bikes registered in Zone A generally attract higher insurance premiums.

1. Zone A

Delhi / NCR

Mumbai

Kolkata

Chennai

Bengaluru

Hyderabad

2. Zone B

Rest of the cities in India

Source: IRDAI Motor Insurance Tariff

Higher Risk of Two-Wheeler Accidents in Metro Cities

Urban and metro cities have a higher likelihood of road accidents and greater risk exposure compared to rural and smaller towns. Dense traffic, congested roads, and a high concentration of vehicles significantly increase the chances of collisions involving two-wheelers. Riders in metro areas frequently navigate crowded intersections and stop-and-go traffic conditions, which raises the probability of both own-damage and third-party insurance claims.

Urban vs Rural Risk for Two-Wheeler Riders

| Risk Type | Metro / Urban Areas | Rural Areas |

|---|---|---|

| Theft | Extremely high; cities such as Delhi record over 1 lakh vehicle theft cases annually, making them major hotspots. | Lower theft risk due to lower vehicle density and stronger community surveillance. |

| Pollution | Severe exposure; riders in major cities face PM2.5 levels 4–5× higher than WHO safe limits. | Pollution exposure is significantly lower. |

| Accident Frequency | Very high due to dense traffic, signal intersections, and frequent stop-and-go riding. | Lower accident frequency because of lighter traffic movement. |

| Maintenance | Higher due to frequent braking, clutch usage, and idling in traffic. | Lower because of steady riding speeds and less congestion. |

Increased Bike Theft Rates in Urban Areas

Bike theft is more common in metro cities due to the high concentration of vehicles and easier resale opportunities in large urban markets. Because theft-related claims occur more frequently in these areas, insurers often charge higher premiums for comprehensive bike insurance, especially for popular commuter motorcycles.

According to the Delhi Police Annual Crime Report 2023, the city recorded over 44,000 vehicle theft cases, with two-wheelers accounting for the majority of stolen vehicles. High theft incidence in metro cities is one of the major risk factors insurers consider while calculating bike insurance premiums.

Source: Delhi Police Crime Branch – Annual Crime Report 2023.

Expensive Repairs and Labour Costs in Tier 1 Cities

Repair costs for two-wheelers are generally higher in metro cities because authorised service centres, spare parts, and skilled labour charges are more expensive in Tier-1 locations. Since insurers anticipate higher repair payouts for claims in these cities, they factor these costs into premium calculations for bike insurance.

Industry estimates from the Indian automotive aftermarket sector indicate that labour charges in metro cities can be about 20–30% higher than in smaller towns, which contributes to higher claim costs for insurers. Source: Automotive Aftermarket Industry Reports (India)

Higher IDV and Premium Bike Ownership in Metro Cities

Metro cities tend to have a higher concentration of premium and high-value motorcycles, which leads to a higher Insured Declared Value (IDV) for these vehicles. Since insurance premiums are calculated based on the bike’s IDV, higher-value bikes in metro areas typically result in higher insurance premiums compared to smaller cities or rural regions.

Two-Wheeler Usage Patterns in Metro Cities

Two-wheelers in metro cities are typically used more intensively, which increases vehicle wear, accident exposure, and the probability of insurance claims.

Daily long-distance commuting

Stop-and-go traffic conditions

Commercial usage

Many riders travel longer distances for work, increasing road exposure and accident risk.

Frequent braking, clutch use, and congestion lead to higher wear and tear on the bike.

Two-wheelers are widely used by delivery and gig workers, which increases daily mileage and claim probability.

Why Add-On Covers Increase Premiums in Metro Cities

Riders in metro cities often choose additional coverage to protect their bikes against higher urban risks, which increases the overall insurance premium.

Zero Depreciation Cover

Engine Protection Cover

Roadside Assistance (RSA)

Return-to-Invoice Cover

Popular in cities because it covers the full cost of replaced parts without depreciation deductions.

Useful in metros prone to waterlogging and heavy rainfall, which can damage the engine.

Frequently chosen due to traffic congestion and higher chances of breakdowns during daily commuting.

Preferred for new and high-value bikes to recover the full invoice value in case of total loss or theft.

Can You Reduce Bike Insurance Premium Even in a Metro City?

Yes, even in metro cities where premiums are typically higher, riders can still reduce their bike insurance costs through smart policy choices. Maintaining a No Claim Bonus (NCB), choosing a higher voluntary deductible, and installing ARAI-approved anti-theft devices can help lower premiums. Comparing policies online and selecting only necessary add-ons can also make the policy more affordable.

Conclusion - Metro City Living Comes With Higher Insurance Risk

While TP bike insurance rates remain constant, having comprehensive bike insurance in metro cities (specifically zone A cities) is more expensive than in other cities (Zone B). This is because of risk assessment done by the insurer, as metro cities pose a higher risk than rural or other urban centres. However, you can always plan and structure your policy to fit your budget, and save money by keeping a cleaner riding record, claim NCBs, and have better peace of mind.

Also Read:

Disclaimer: Discounts on bike insurance premiums are subject to the insurer and may vary across different insurers. Not all insurers provide discounts for clean riding records; check your policy carefully.

FAQs on Higher Bike Insurance Premiums in Metro Cities

Why does my bike insurance premium change when I move cities?

Premiums vary by location because insurers assess risk based on accident rates, theft frequency, and repair costs in the city of registration.

Are all metro cities treated the same for bike insurance pricing?

Most insurers classify major metros under Zone A, but the final premium may still vary slightly depending on the insurer and policy features.

Is third-party bike insurance also costlier in metro cities?

No. Third-party premiums are fixed by IRDAI, so they remain the same across all cities in India.

Does installing an anti-theft device reduce premiums in metros?

Yes. Installing an ARAI-approved anti-theft device can reduce the own damage premium.

Can NCB reduce the impact of metro city pricing?

Yes. A No Claim Bonus (NCB) can provide up to 50% discount on the own damage premium after five claim-free years.

Does bike insurance premium differ by PIN code within a city?

Premiums are mainly based on zone classification (city level) rather than individual PIN codes.

What are Zone A cities in bike insurance?

Zone A includes major metro cities such as Delhi/NCR, Mumbai, Kolkata, Chennai, Bengaluru, Hyderabad.

What are Zone B cities in bike insurance?

Zone B includes all other cities and towns in India that are not part of the Zone A classification.

Does bike type affect insurance premiums in metro cities?

Yes. Engine capacity, bike value, and model popularity influence the premium, with higher-value bikes generally attracting higher premiums.

in Bikes.webp)

in Bikes.webp)