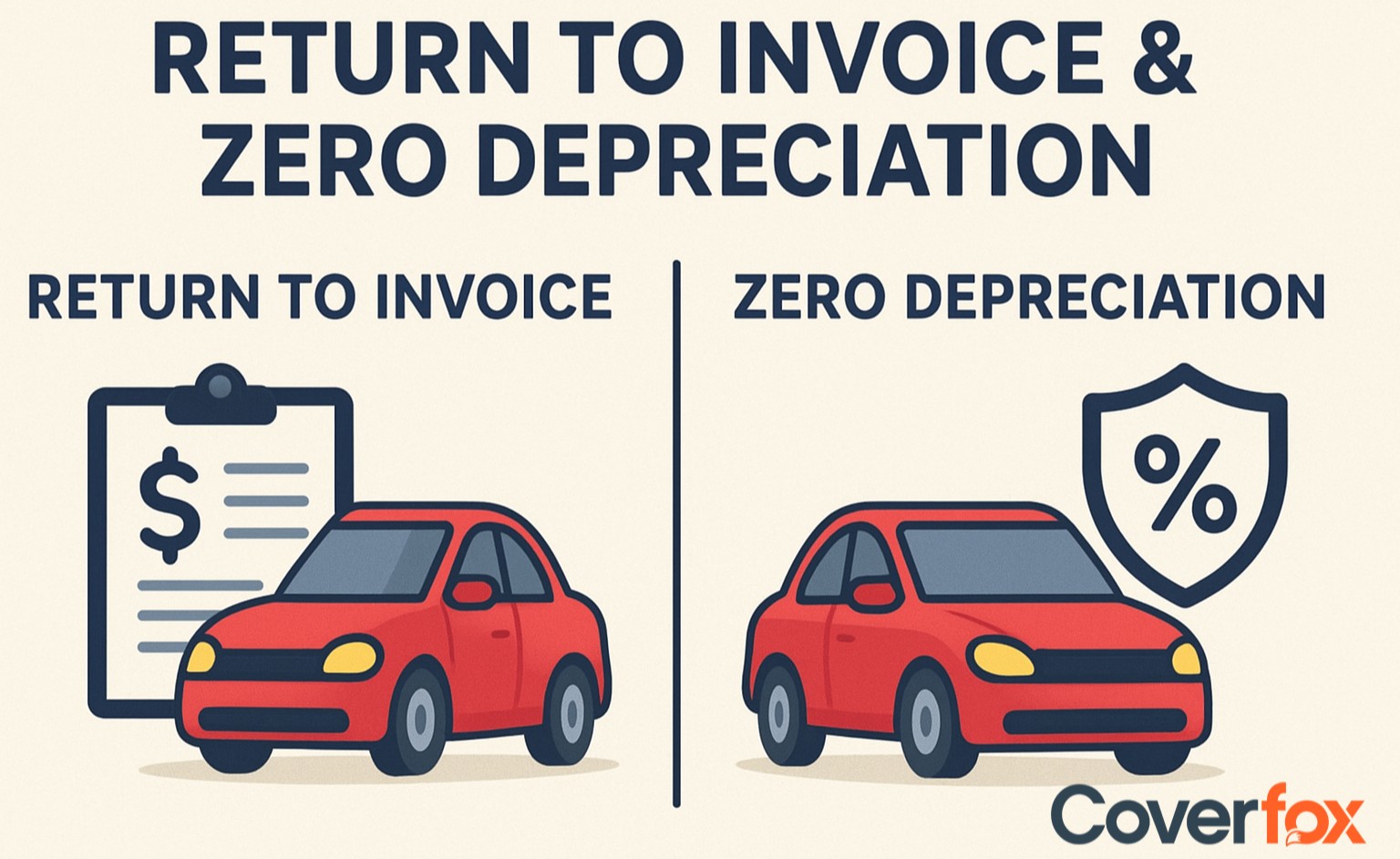

Zero Depreciation and Return to Invoice (RTI) are essential motor insurance add-ons that enhance your financial protection beyond standard coverage. While Zero Dep covers repair and replacement costs without accounting for depreciation, RTI ensures you receive your car’s full invoice value in case of total loss or theft. Choosing between them depends on your car’s age and usage - or you can opt for both for maximum protection.

Driving on Indian roads without a motor insurance policy can land you in legal trouble, as it is mandatory to have a third-party insurance policy to drive legally in India. However, a TP policy does not give complete financial protection to your vehicle, making comprehensive car insurance a better choice. Still, neither TP nor comprehensive insurance can cover depreciation costs or the invoice value of the vehicle. That's where add-ons kick in. Add-ons like Zero Depreciation Cover and Return to Invoice Cover are crucial add-ons in motor insurance, and this article will talk about their significant differences.

Understanding Insurance Add-ons - Car and Bike Insurance

Add-ons in motor insurance enhance your protection and coverage. These include zero depreciation, roadside assistance, engine protection, key protector, return to invoice cover, etc, each having its own significance. However, amongst them, zero depreciation cover and return to invoice cover stand out significantly, as they directly address the value of the car. While add-ons do sound nice to the ears, they do come at an additional cost. Although minimal, they do add up to the total premium cost of your car or bike insurance. So choose your add-ons wisely.

What is Zero Depreciation Cover?

Zero Depreciation Cover, also known as Nil-depreciation cover or bumper-to-bumper cover, is a common add-on in motor insurance that deals with the depreciation of the vehicle parts. While settling a claim, you do not receive the complete value of the vehicle’s parts (such as rubber parts, fibreglass, plastic parts, etc); instead, it is calculated based on the depreciation of the car. This add-on is available for cars up to 5 years old (Some insurers allow up to 7 years old), and you can make a limited number of zero depreciation claims in a policy year (varies by insurer).

NOTE: Zero Depreciation does not provide 100% coverage; standard deductibles still apply, and this add-on is slightly more expensive than a standard car insurance policy.

What is Return to Invoice (RTI) Cover?

Return to Invoice Cover ensures you get your car’s original invoice value (including ex-showroom price, road tax, and registration) if it’s stolen or declared a total loss. Normally, insurers pay the depreciated Insured Declared Value (IDV), but RTI eliminates that deduction. It’s available for cars usually under 3–5 years old and offers benefits like full value reimbursement, but doesn’t apply to partial losses or repairs.

Key Differences Between Zero Depreciation and Return to Invoice

Here is a table showcasing the differences between zero depreciation vs return to invoice covers:

| Parameter | Zero Depreciation Cover | Return to Invoice (RTI) Cover |

|---|---|---|

| Meaning | Covers the full claim amount without deducting depreciation on replaced car parts. | Pays the car’s original invoice value (ex-showroom + registration + road tax) in case of total loss or theft. |

| Applicability | Applicable for repair-related claims where parts are replaced. | Applicable only in case of total loss or theft of the vehicle. |

| Ideal For | Cars less than 5 years old that undergo regular repairs or replacements. | New cars (usually under 3–5 years old) are vulnerable to theft or major damage. |

| Claim Settlement | You get the complete cost of replaced parts without depreciation deductions. | You receive the full invoice value of the car instead of its depreciated IDV. |

| Premium | Slightly higher than standard comprehensive policy. | Higher than Zero Depreciation due to full value reimbursement. |

| Coverage Duration | Renewable annually; valid till the car is around 5 years old. | Available for new cars up to 3–5 years, depending on insurer policy. |

| Main Exclusion | Doesn’t cover tyres, tubes, batteries, or regular wear and tear. | Not applicable for partial losses, repairs, or minor damages. |

| Best Suited For | Owners who want minimal repair costs and maximum claim value. | Owners of new or high-value cars seeking total financial protection. |

Which One Should You Choose - RTI Cover or Zero Dep Cover?

Your choice depends on your car’s age, usage, and risk exposure. RTI Cover offers complete reimbursement for total loss or theft, while Zero Depreciation Cover protects you from depreciation deductions during repairs.

1. For New Cars (Under 3 Years) – Choose RTI Cover

RTI is ideal for new vehicles as it reimburses the full invoice value, including taxes and registration, if your car is stolen or completely damaged.

Example: If your new car, worth ₹12 lakh, is stolen, standard insurance may pay ₹10 lakh (after depreciation). With RTI, you get the full ₹12 lakh — no value loss.

2. For Cars Between 3–5 Years – Choose Zero Depreciation Cover

Zero Dep Cover ensures you get the full repair cost without deductions for part depreciation, perfect for cars with moderate wear and tear.

Example: If your 4-year-old car sustains ₹1 lakh damage, a standard policy may pay only ₹75,000 after depreciation. With Zero Dep, you receive the full ₹1 lakh. (You may still have to pay deductibles.)

Can You Buy Both Add-ons Together - RTI Cover and Zero Dep Cover?

Yes, in fact, this is a very sure-shot way of protecting your prized possession. You can buy both RTI and Zero Depreciation covers together for complete protection. Zero Dep covers repair and part replacement costs without depreciation, while RTI ensures full invoice value in case of total loss or theft. Many insurers allow bundling both, with a slightly higher premium but far greater financial security.

How to Add Zero Depreciation or RTI to Your Policy?

Coverfox serves as an excellent platform for all your motor insurance needs. From buying car/bike insurance, to customisation of the policy, and to comparing different insurers all can happen at one place. To buy RTI Cover or nil-depreciation cover, all you need to do is go over to car insurance plans, and select the respective add-on from the available drop-down list on the page!

Key Takeaways

Add-ons are your key to enhancing your insurance coverage. Zero depreciation cover ensures the depreciating costs of your parts are reimbursed at full value, whereas RTI cover ensures you receive the entire amount you paid for the vehicle, which includes on-road price, tax and registration charges. RTI Cover is more expensive than zero-depreciation cover, but provides further protection of assets. Choose your add-ons smartly, as they do add up to the premium cost of motor insurance.

Related Articles:

Frequently Asked Questions

Is Zero Depreciation better than Return to Invoice add-on?

Not necessarily — Zero Dep covers repair costs without depreciation, while RTI pays the full invoice value for total loss or theft. The better option depends on your car’s age and needs.

Are Zero Dep and RTI the same?

No, they serve different purposes. Zero Dep covers part replacement costs, while RTI compensates the entire invoice value if the car is stolen or declared a total loss.

Does Zero Dep cover engine parts?

Yes, engine and gearbox parts are covered under Zero Dep if the damage is caused by an insured event, not wear and tear or oil leakage.

Does RTI include road tax and registration cost?

Yes, most RTI covers reimburse the on-road price, which includes the car’s invoice value, registration charges, and road tax.

Is RTI available for cars older than 3 years?

Typically no — RTI is usually available only for new cars up to 3 years old. Some insurers may extend it up to 5 years with conditions.

Can we add Zero Depreciation cover with own-damage bike insurance?

Yes, most insurers allow adding Zero Dep to comprehensive or standalone own-damage bike insurance policies.

Are all parts of the bike covered under Zero Depreciation?

Almost all, including metal, plastic, and fibre parts, are covered without depreciation; however, tyres, tubes, and batteries may have limited coverage.

What are the exclusions under the RTI cover?

RTI doesn’t cover partial damages, normal wear and tear, or cars older than the eligible age (usually 3 years).

Is RTI good for car insurance?

Yes, it’s valuable for new cars as it ensures you receive the full invoice amount in case of theft or total loss, minimising your financial loss.