Explore the world of auto insurance with our in-depth IDV (Insured Declared Value) tutorial. Learn its significance, calculation methods, and why it's crucial for your coverage decisions. Get clarity on the terms and ensure adequate protection for your vehicle.

When it comes to car insurance, there are many terms and acronyms that can be confusing for the average person. One of these terms is IDV, which stands for "Insured Declared Value". Understanding what IDV is and how it affects your car insurance policy is crucial for making informed decisions about your coverage. In this article, we'll break down everything you need to know about IDV in car insurance.

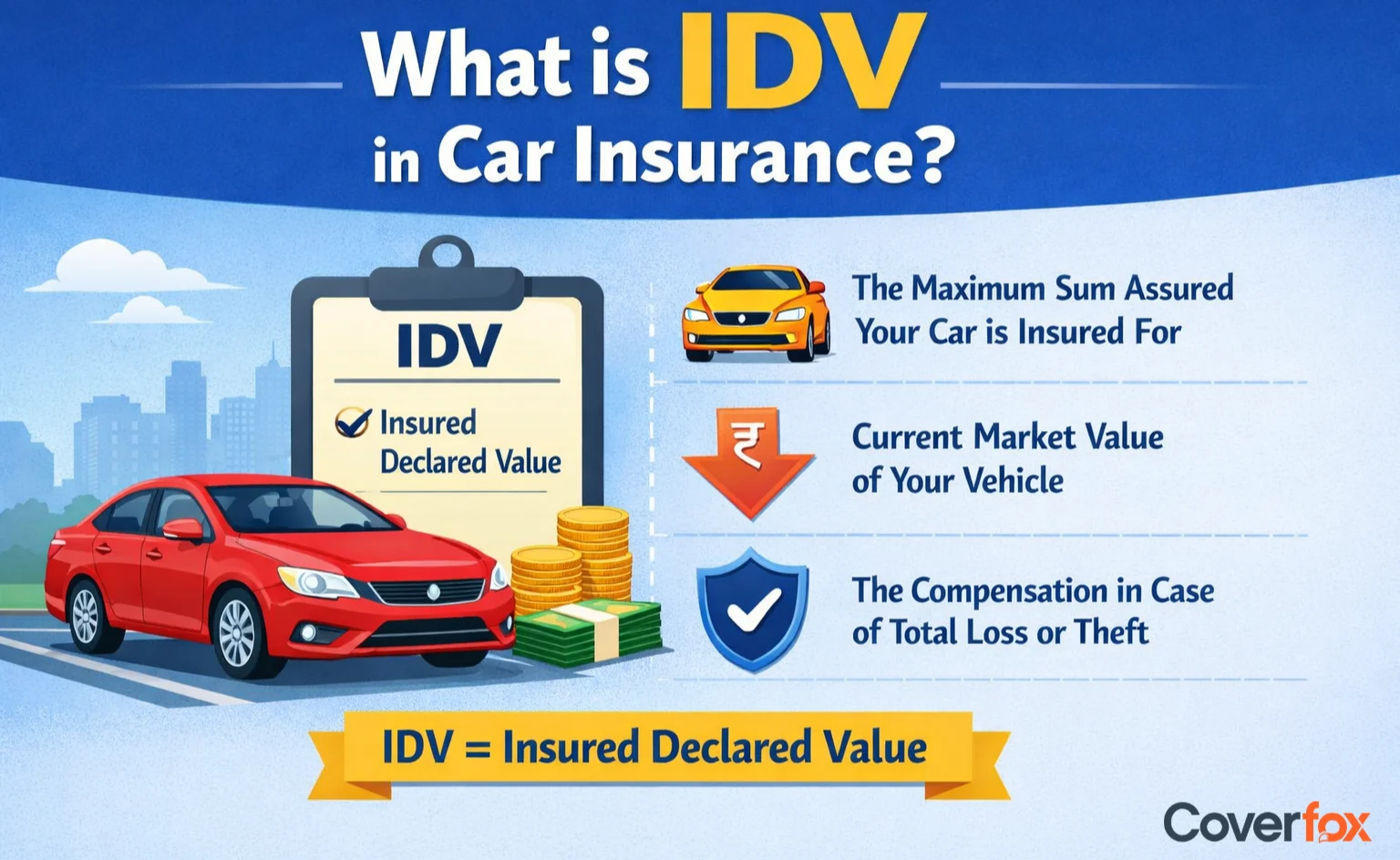

What is IDV?

Understanding the Basics

Before we dive into IDV, let's first understand the basics of car insurance. Car insurance is a type of insurance that provides financial protection against physical damage or bodily injury resulting from traffic collisions and against liability that could also arise from incidents in a vehicle. In exchange for paying a premium, the insurance company agrees to cover the costs associated with these incidents.What is IDV?

IDV, or Insured Declared Value, is the maximum amount that an insurance company will pay in case of a total loss or theft of your vehicle. In simpler terms, it is the current market value of your car. This value is determined by the insurance company at the time of purchasing the policy and is calculated based on the manufacturer's listed selling price of the vehicle minus the depreciation value.Why is IDV Important?

Impact on Insurance Premium

The IDV of your car plays a significant role in determining the premium you pay for your car insurance. The higher the IDV, the higher the premium, and vice versa. This is because a higher IDV means a higher coverage amount, which means the insurance company will have to pay more in case of a total loss or theft of your vehicle.Impact on Claim Settlement

In case of an accident or theft, the insurance company will only pay up to the IDV amount. This means that if your car is damaged beyond repair or is stolen, you will only receive the IDV amount as compensation. Therefore, it is essential to have an accurate IDV to ensure that you are adequately covered in case of such incidents.How to calculate IDV for car insurance

Insured Declared Value (IDV) is the maximum value that an insurance company is liable to pay you in case of total loss of your vehicle. The IDV of your car depends on the manufacturer's listed selling price of the model of the car and the brand. Higher the age of the car, higher would be the depreciation percentage too. This amount of the depreciation is fixed.

In short,

IDV = Manufacturer's listed selling price or Ex-showroom price x Depreciation factor

Remember that a car that is new will always have the maximum IDV, but will gradually lower down due to depreciation.

Mentioned below are the standard rates of depreciation specified by the Motor Tariff Act:

| Your Car's age | % Of Depreciation For Calculating IDV |

|---|---|

| Up to 6 Months | 5% |

| 6 Months to 1 Year | 15% |

| 1 - 2 Years | 20% |

| 2 - 3 Years | 30% |

| 3 - 4 Years | 40% |

| 4 - 5 Years | 50% |

The IDV of the accessories fitted to the car but excluded in the manufacturer's listed selling price is also to be fixed in a similar fashion.

The below mentioned formula summarizes the Insured Declared Value (IDV) in a crisp manner:

IDV = {[(Manufacturer's listed selling price) + (Sales Tax) + (Accessories excluded – depreciation)] – (Depreciation + Registration costs + Insurance costs)}

What is IDV Cover in Car Insurance?

Understanding IDV Cover

IDV cover is an add-on cover that you can purchase along with your car insurance policy. This cover ensures that you receive the full IDV amount in case of a total loss or theft of your vehicle. Without this cover, you may only receive the depreciated value of your car, which can be significantly lower than the IDV.Benefits of IDV Cover

The primary benefit of IDV cover is that it provides you with complete financial protection in case of a total loss or theft of your vehicle. This means that you will receive the full IDV amount, which can be used to purchase a new car or cover any outstanding loans on your previous vehicle.How to Check IDV of Car?

Checking IDV on Your Insurance Policy

The easiest way to check the IDV of your car is to refer to your insurance policy. The IDV is mentioned on the policy document, along with other details such as the premium amount, coverage period, and add-on covers.

Checking IDV Online

If you have purchased your car insurance policy online, you can also check the IDV on the insurance company's website. Most insurance companies have a customer portal where you can log in and view your policy details, including the IDV.

What is IDV in Bike Insurance?

Understanding IDV in Bike Insurance

IDV is not just limited to car insurance; it is also applicable to bike insurance. In bike insurance, IDV is the maximum amount that the insurance company will pay in case of a total loss or theft of your bike. The IDV is calculated based on the manufacturer's listed selling price minus the depreciation value.Importance of IDV in Bike Insurance

Similar to car insurance, the IDV of your bike plays a crucial role in determining the premium you pay and the claim settlement amount. It is essential to have an accurate IDV to ensure that you are adequately covered in case of any incidents.What is the Full Form of IDV in Insurance?

The full form of IDV in insurance is "Insured Declared Value". This term is used in both car insurance and bike insurance and refers to the maximum amount that the insurance company will pay in case of a total loss or theft of your vehicle.

Conclusion

IDV is an essential aspect of car insurance and bike insurance. It determines the maximum amount that the insurance company will pay in case of a total loss or theft of your vehicle. It is crucial to have an accurate IDV to ensure that you are adequately covered and receive the full amount in case of any incidents. Use the IDV value calculator provided by insurance companies to determine the IDV of your vehicle and make informed decisions about your coverage.

Want to learn more about IDV? Watch this cool video!