Prasanna Kumar

Getting car insurance through coverfox has saved me both time & money

09 Jan 2025

Language

Language

Car insurance is a legal contract between the insurer and the policyholder that gives financial protection for your car from damage caused by accidents, mishaps, natural disasters, man-made hazards, theft, etc. In India, as per the Motor Vehicles Act, 1988, having third-party car insurance is mandatory to drive legally on public roads. Driving without car insurance can lead to fines ranging from ₹2,000 to ₹4,000, with higher penalties for repeated offences. With car insurance plans starting from just ₹2,094/year*, you can safeguard yourself against unexpected financial risks while also enjoying benefits like cashless repairs at network garages and reliable claim support from Coverfox.

Car insurance helps you stay compliant on the road, whilst protecting your vehicle financially from damage arising from accidents, natural disasters or man-made hazards. Here's why car insurance is essential for your four-wheeler:

| Feature | Third-Party Car Insurance | Standalone Own Damage Insurance | Comprehensive Car Insurance |

|---|---|---|---|

| What it covers | Legal liability towards third-party injury, death, or property damage. | Damage to your own car caused by accidents, theft, fire, natural or man-made events. | Combines third-party liability and own damage under a single policy. |

| Own vehicle damage | ✗ Not covered | ✓ Covered | ✓ Covered |

| Third-party liability | ✓ Covered | ✗ Not covered | ✓ Covered |

| Theft of an insured car | ✗ Not covered | ✓ Covered | ✓ Covered |

| Fire & natural disasters | ✗ Not covered | ✓ Covered | ✓ Covered |

| Personal Accident Cover | Available as applicable under regulatory provisions. | Available as applicable under regulatory provisions. | Available as applicable under regulatory provisions. |

| Add-on covers | ✗ Not available | ✓ Available | ✓ Available |

| No Claim Bonus (NCB) | ✗ Not applicable | ✓ Applicable | ✓ Applicable |

| Who can buy it? | Any car owner. Mandatory for driving on public roads. | Car owners who already have a valid Third-Party policy. | Any car owner looking for complete protection. |

| Legal requirement | Mandatory under the Motor Vehicles Act. | Optional. Cannot replace the mandatory Third-Party cover. | Optional, but fulfils the Third-Party insurance requirement as it includes it. |

| Premium | Lowest | Moderate | Higher, reflecting wider coverage. |

| Best suited for | Owners looking to meet the minimum legal requirement. | Owners with an active Third-Party policy who want protection for their own car. | Owners seeking the broadest protection against both third-party liabilities and damage to their own vehicle. |

Swipe left/right to see all plans →

Electric vehicle (EV) insurance is a car insurance policy designed specifically for electric cars. Like a regular car insurance policy, it provides third-party liability and own-damage coverage. In addition, it covers EV-specific components such as the battery, electric motor, charging equipment, and electrical circuitry, subject to the policy's terms and conditions.

Electric car sales are gradually increasing in India. In fact, according to the International Energy Agency (IEA), electric car sales in India grew by 78% year-on-year in 2025, reaching 165,000 units and accounting for nearly 4% of total car sales. This evidently shows the need for electric car insurance in India.

Many insurers offer EV-specific add-ons such as battery protection cover, roadside assistance, charging equipment cover, and zero depreciation cover to provide broader protection. In addition, several state governments offer incentives for EV ownership, such as road tax exemptions or concessions and registration fee waivers, making electric vehicles more affordable to own in India.

Note: Inclusions and Exclusions of a policy are subject to the car insurer.

Add-on covers in car insurance online are optional enhancements that you can include with your comprehensive or standalone own-damage policy. Though they come at a small additional cost, these add-ons significantly boost the protection offered by your standard insurance plan. Here are some popular add-ons you can consider:

No Claim Bonus (NCB) Protect is an add-on that protects your No Claim Bonus even after you make an admissible claim during the policy period, subject to the insurer's terms. Since insurers reward every claim-free policy year with an NCB discount of up to 50% on renewal premiums, this add-on helps you preserve that benefit while still raising a claim when needed.

You have earned a 50% NCB (₹5,000 discount) after 5 claim-free years. Unfortunately, you need to file a claim this year.

Standard Renewal Premium: ₹10,000

Although comprehensive car insurance protects your car from damage, it does not cover damage done to your car's engine (unless it is damaged in an accident). A car engine is an expensive part to repair/replace. Hence, opting for an Engine Protection Cover reduces the financial risk. If you opt for this rider, your car engine will be insured as well from damage like water ingress and oil leakage.

Your car gets waterlogged during heavy rains, and the engine suffers internal damage.

Estimated engine repair cost: ₹85,000

This cover is also called a Nil Depreciation cover, or Bumper-To-Bumper car insurance. In this add-on, you receive the full claim amount regardless of car depreciation on the car parts. This helps you get a complete payout and is extremely beneficial for newer cars. It is important to note that zero depreciation coveris only available for cars not older than 5-7 years (depending on the insurer), and only limited zero-dep claims can be made during a policy year. This add-on covers major components such as metal, fibre, and plastic parts, while tyres, tubes, and batteries are covered at 50%.

Your car meets with an accident and multiple parts need replacement.

Total repair cost: ₹48,000

Glass parts: ₹12,000 · Fibre parts: ₹8,000 · Tyres: ₹6,000 · Tubes: ₹2,000 · Battery: ₹5,000 · Plastic/Rubber: ₹7,000 · Metal parts: ₹8,000

Note: Insurer will pay a fixed percentage of the cost of new parts as per IRDAI norms.

Consumables Cover is an add-on that covers the cost of consumable items used during the repair of your insured car, which are typically excluded under a standard car insurance policy. It pays for items such as engine oil, lubricants, nuts, bolts, screws, washers, and similar consumables, helping reduce your out-of-pocket repair expenses after an insured event.

Your car meets with an accident and requires repairs, along with the replacement of consumables.

Total repair cost: ₹22,000

Spare parts (covered normally): ₹15,000 · Consumables (oil, coolant, nuts, etc.): ₹7,000

In a situation where your car key is damaged or lost, it may cost you upwards of ₹10,000 to replace it. This becomes an out-of-pocket expense unless you have Key Protection Cover. This add-on will get you reimbursement for the replacement car key that you will receive from the company's service centre.

You lose your car key, or it gets stolen, and you need an expensive smart key replacement.

Total replacement cost: ₹16,000

A Personal Accident Cover (PA) in car insurance is a type of financial protection where the owner-driver of the insured vehicle is covered if they suffer from bodily injury, partial or permanent disability, or lose their life in a road accident. This is a mandatory cover if you do not already have it, and covers at least ₹15 lakh sum insured for medical expenses/family security.

You meet with an accident that leads to a permanent disability.

Sum insured under PA cover: ₹15,00,000

Roadside Assistance Cover (RSA) in car insurance is an emergency service where you can avail of a towing facility in case your four-wheeler is stuck or inoperable, and you are stranded. Issues like flat tyres, running out of fuel, and battery failures are where RSA cover comes in handy. It is especially beneficial for EV owners who are concerned about their battery range.

Your car breaks down late at night due to a battery failure.

Cost of assistance (towing + service): ₹4,500

If you are purchasing a new car, choosing the right insurance for a new car, especially along with a Return to Invoice (RTI) cover, is highly beneficial. RTI cover ensures you get the original invoice value of your car in case of theft or total loss. This claim amount is inclusive of ex-showroom price, road tax and any registration charges (depending on the insurer). This add-on ensures your prized possession's value is maintained even after initial purchase.

Your car gets stolen within a year of purchase.

Invoice value: ₹10,00,000 · Current IDV: ₹8,20,000

Pay as you drive or PAYD cover is a usage-based add-on where your premium is determined based on how much your car travels (number of km driven during the policy term). This is useful for those who do not use their car often and still need car insurance protection.

You drive your car only for short trips (approx. 5,000 km/year).

Standard Premium: ₹12,000

Disclaimer: The availability, features and eligibility criteria of add-on covers may vary across insurers and policy types. Please refer to the policy wording for complete details.

Online car insurance prices vary for each policy. Every car insurance policy is customised, and the premium depends on various factors. Here are the major components in calculating a car insurance premium:

Suppose you own a 2024 Maruti Suzuki Baleno Zeta Petrol, registered in Mumbai, and you're buying a comprehensive car insurance policy.

The premium is calculated as follows:

Final Premium = Own Damage Premium + Third-Party Premium + Add-on Premium − NCB Discount + GST (18%)

| Premium Component | Calculation | Amount |

|---|---|---|

| Own Damage Premium | Approximately 1.8% of IDV (varies by insurer and risk profile) | ₹12,600 |

| Third-Party Premium | As applicable for the vehicle category under regulatory rates | ₹2,100 |

| Zero Depreciation Add-on | Optional cover | ₹2,000 |

| Gross Premium | Own Damage + Third Party + Add-on | ₹16,700 |

| Less: No Claim Bonus (20%) | 20% of Own Damage Premium (₹12,600) | −₹2,520 |

| Premium Before GST | ₹14,180 | |

| GST @18% | 18% of ₹14,180 | ₹2,552 |

| Final Premium Payable | ₹16,732 | |

Note: This is only an illustrative example to explain how a car insurance premium is calculated. The own-damage premium is not fixed and differs across insurers based on factors such as the car's make and model, age, IDV, registration location, claim history, and selected add-ons. Third-party premium is charged as per the applicable regulatory rates for your vehicle category.

The table below gives a broad idea of how premiums may vary across different vehicle categories.

| Vehicle Type | Approximate Annual Premium |

|---|---|

|

Hatchback

|

₹2,500 – ₹8,000 |

|

Sedan

|

₹3,500 – ₹12,000 |

|

SUV

|

₹5,000 – ₹20,000+ |

Disclaimer: These figures are indicative for comprehensive car insurance. The new car insurance price depends on factors such as the car's IDV, make and model, age, location, and the add-ons you choose.

Car insurance premiums are influenced by the following factors:

IDV (Insured Declared Value) is the estimated market value of your car determined by the insurer at the time of purchasing or renewing the 4 wheeler insurance. Think of it as the insured value of your vehicle — the maximum amount the insurer will pay if your car is stolen and not recovered or is damaged beyond economic repair (total loss).

The IDV is calculated using the vehicle's manufacturer's listed selling price (excluding registration charges and road tax) after applying depreciation based on the car's age. For vehicles older than five years, insurers usually arrive at the IDV through mutual agreement with the policyholder, considering the vehicle's condition, mileage, and prevailing market value.

Example

Suppose you purchased a car for ₹10 lakh. After three years, its value has reduced because of depreciation. At renewal, the insurer determines its IDV to be ₹7 lakh.

If the car is stolen and cannot be recovered, or the repair cost exceeds the insurer's total-loss threshold, your claim settlement will be based on this ₹7 lakh IDV, subject to the policy's terms and applicable deductions.

The depreciation applied while calculating the IDV depends on the age of the vehicle.

| Age of the Vehicle | Depreciation Applied |

|---|---|

| Up to 6 months | 5% |

| 6 months to 1 year | 15% |

| 1 year to 2 years | 20% |

| 2 years to 3 years | 30% |

| 3 years to 4 years | 40% |

| 4 years to 5 years | 50% |

| More than 5 years | Decided by mutual agreement between the insurer and policyholder based on the vehicle's condition and market value. |

Note: The depreciation percentages above are the standard rates used for calculating IDV under Indian motor insurance guidelines.

Lowering your car insurance premium doesn't necessarily mean you have to give up on crucial coverage. Here are some tips that will help you reduce your car insurance premium without compromising on your coverage:

Every claim-free year earns you a discount on the own-damage premium. The longer you avoid making own-damage claims, the bigger the savings at renewal.

A higher voluntary deductible lowers your premium because you agree to bear a larger share of the repair cost if you make a claim.

Add-ons increase your premium, so select only those that match your car's age, usage, and your coverage needs instead of opting for every available cover.

Setting the IDV much higher than your car's market value increases the premium, while setting it too low reduces your claim amount. An accurate IDV gives you the right balance between cost and coverage.

Many insurers offer a discount on the own-damage premium for cars fitted with certified anti-theft devices.

Timely renewal helps you retain your No Claim Bonus and prevents unnecessary premium increases caused by a break in insurance coverage.

The premium and coverage offered for the same car can vary across insurers. Comparing different plans helps you choose a policy that offers the protection you need at a price that fits your budget.

Cover AI analyses policy documents, compares plans, and highlights differences in coverage and add-ons. This helps you choose a policy that fits your needs instead of paying extra for features you may never use.

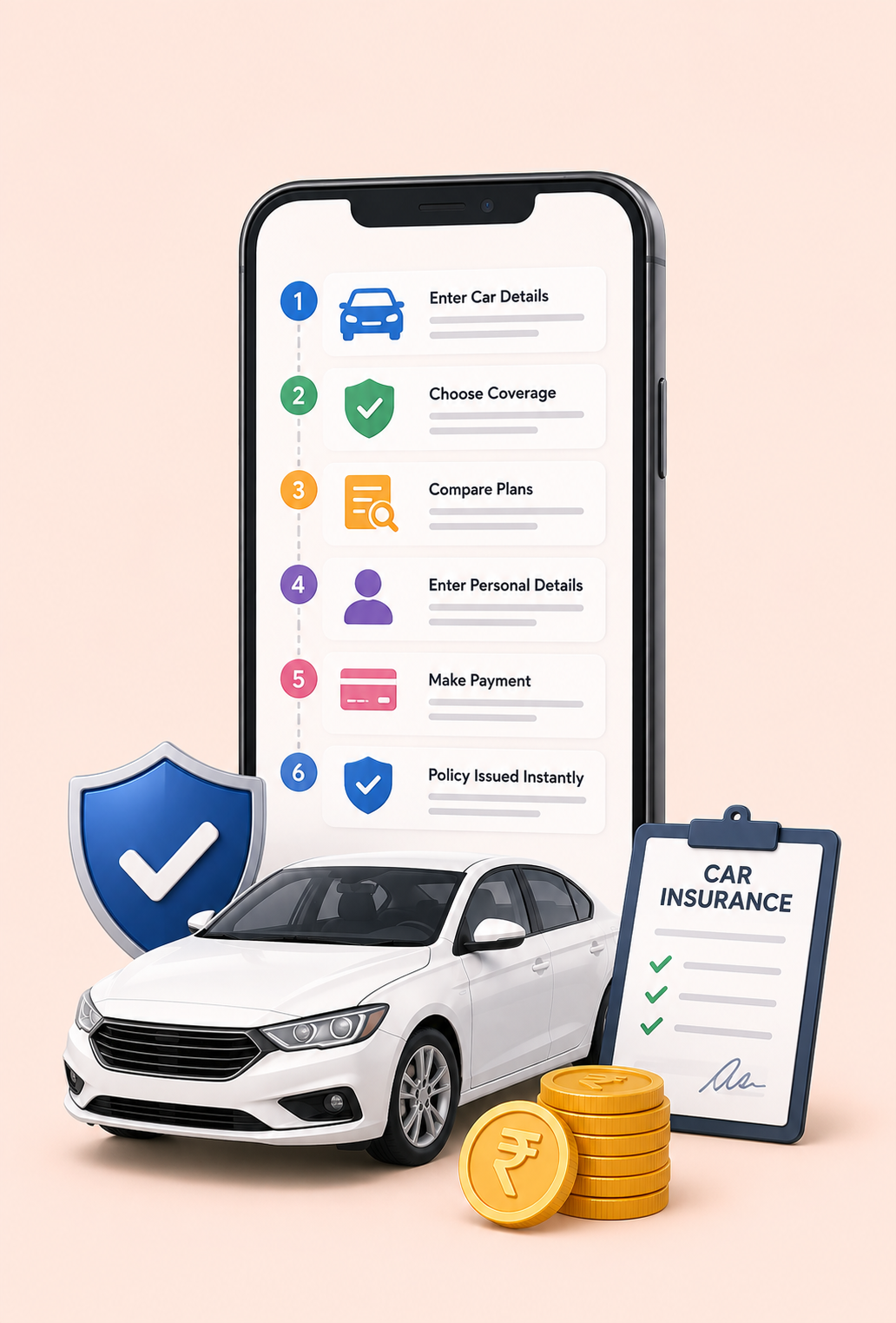

Buy car insurance online from Coverfox to get the best car insurance policy that will suit your budget and cover all your needs. Follow these simple steps to purchase four-wheeler insurance online:

Provide your car's registration number, make, model and registration location to get quotes.

Click on "Get Quotes" to compare plans from different insurers, and select add-ons that fit your requirements.

Choose your plan, pay securely, and get your insurance policy for car in under 3 minutes.

Pro Tip: You can consult with Cover AI to check if your policy is good enough or requires any upgrade/update.

You can buy new car insurance for your brand new car by following these simple steps:

Click on "Bought a new car?" and add in your car details like make, model and registration.

Click on "Get Quotes" and compare new car insurance policies by India's top car insurers. Get multi-year third-party and OD cover under bundled new car insurance.

Review your 4-wheeler policy and buy insurance online through the secure payment gateway. Get your policy delivered instantly to your registered email.

You can save up to 85%* when comparing car insurance online. Here are the benefits of buying car insurance online:

Car insurance policy renewal is essential to keep your policy active, avoid a coverage gap, and continue enjoying uninterrupted coverage. It also helps you retain your No Claim Bonus (NCB), avoid vehicle re-inspection in most cases, and enjoy applicable renewal benefits.

You can complete car insurance online renewal through Coverfox quickly and without any hassle:

Enter your Previous Car Insurance Details

Add your previous policy information like policy number, expiry details and whether you have made a claim or not.

Compare Car Insurance Renewal Quotes

Compare different plans and car insurance renewal prices before renewing your existing policy. The best time to upgrade your car policy is during renewal.

Renew in under 3 minutes!

Complete your car policy renewal or buy a new policy, pay through our secure payment gateway, and get your renewed car insurance policy in under 3 minutes.

Pro Tip: Before renewing car insurance, find policy gaps on Cover AI. Renewals are the best time to upgrade your car insurance policy, set a new IDV, add or remove add-ons, and utilise the NCB benefit.

Renewing your car insurance before it expires keeps your coverage active and ensures you continue to enjoy all your policy benefits.

If your car insurance has expired, your vehicle is no longer covered from the day the policy lapses. Any accident, theft, or damage that occurs during this period will not be covered by the insurer. In addition, driving without a valid third-party insurance policy is a violation of the law.

Although the policy expires immediately, insurers allow a grace period of up to 90 days to retain your No Claim Bonus (NCB), subject to the insurer's terms and applicable guidelines. If you renew after the policy has lapsed, the insurer may require a pre-renewal vehicle inspection before issuing a new policy. Renewing your car insurance at the earliest helps restore your coverage, preserve your NCB, and avoid unnecessary delays in the renewal process.

No claim bonus in car insurance is offered to policyholders who have claim-free policy years. This benefit builds up over the years and fetches you discounts on own-damage premiums. Note that NCB benefit does not apply to third-party premiums. Here's how NCB build up over the years for car insurance renewals:

| Claim-Free Policy Years | NCB Discount on Own Damage Premium |

|---|---|

| After 1st claim-free year | 20% |

| After 2nd consecutive claim-free year | 25% |

| After 3rd consecutive claim-free year | 35% |

| After 4th consecutive claim-free year | 45% |

| After 5th consecutive claim-free year and onwards | 50% (Maximum) |

Note: Although this is standard for insurers, availability and amount of NCB remain at the discretion of the insurers.

Choosing the right car insurance policy involves more than comparing premiums. The insurer, policy type, coverage, and add-ons all play a role in determining how well your car is protected and how much you pay. Here are factors to consider before buying or renewing your 4-wheeler insurance.

If your car is driven regularly, a comprehensive policy usually makes more sense than buying only the mandatory third-party cover.

Two policies with similar premiums can offer very different benefits. Compare the coverage, exclusions, deductibles, and optional add-ons before making a decision.

A policy is only as good as the support you receive during a claim. Looking at the insurer's claim settlement record and customer experience can help you choose the best insurance for car.

Having a network garage close to your home or workplace is an important factor when choosing the right insurance for a car, as it can make repairs quicker and reduce out-of-pocket expenses during a claim.

An IDV that's too low can reduce your claim amount, while an inflated IDV only increases the premium. A realistic value gives you the right balance.

Every policy has situations that aren't covered. Spending a few minutes reading the exclusions today can prevent confusion when raising a claim later.

A brand-new car and a ten-year-old hatchback rarely need the same level of protection. Choose add-ons based on your vehicle and driving conditions rather than selecting every available option.

Instead of opening multiple insurer websites, compare plans on Coverfox to see differences in premiums, benefits, network garages, and policy features in one place. If you're unsure which policy suits you better, Cover AI can help explain the differences in plain language.

Use Cover AI to get advice on what policy fits your budget and requirements. Try Cover AI now on ai.coverfox.com

Trusted by over a million customers for buying and renewing car insurance across India.

Explore plans from leading insurance companies in one place and choose the policy that best meets your needs and budget.

The premium you see is the premium you pay. Compare quotes with complete clarity, make informed decisions and pay using the secure gateway.

From policy purchase and renewals to claim-related queries, our support team is available whenever you need assistance.

Buy or renew your car insurance online in minutes and receive your policy digitally without lengthy paperwork.

Renew your existing policy or switch to another insurer seamlessly while retaining eligible benefits such as your No Claim Bonus.

Compare policies, understand coverage, decode policy wordings, and get instant answers to your insurance questions, all powered by Cover AI.

Try COVER AI

Knowing how to make a car insurance claim will help you in the time of need. The claim process is simple, and following the required steps can make the experience smoother and avoid any delays. Car insurance claims can be made in 2 ways:

Where you repair your car decides how the claim is settled.

If your car requires repair due to an insured event, take it to your insurer-approved network garage for repairs. Before the repairs, fill the claims form and the insurer will approve the claims as per the policy terms, and will settle the bill directly with the network garage. In this scenario, you do not need to pay the bill upfront, as it will be settled by the insurer (only deductibles and uninsured repairs will have to be paid by you).

In this type of car insurance claim, once an insured event happens (accident, theft, damage due to natural disasters, etc), get your car fixed at a non-network garage. Once the car is fixed, take the repair bill and submit the claims form with your insurer to get reimbursement for the repairs made. The claim amount will be reimbursed into the policyholder's account as per policy terms after claim approval.

The process is the same for both claim types until settlement.

Report the accident, theft, or damage as soon as possible through the insurer's helpline, website, or mobile app.

Take clear photographs or videos of the damage, note the location, and collect details of any third parties involved. In case of theft, major accidents, or third-party injuries, file an FIR with the police.

Provide your policy details, RC, driving licence, claim form, photographs, FIR (where applicable), and any other documents requested by the insurer.

The insurer will appoint a surveyor to inspect the damage and assess the claim before repair work begins, unless the inspection requirement is waived.

Pick the path that suits you — see the cashless and reimbursement steps below.

Note: The steps outlined above are for general guidance. The actual claim process, documentation, and timelines may differ across insurers and policy types.

Quick answers to the most common questions about car insurance policies, claims, and renewals.

If you bought your policy through Coverfox, log in to your Coverfox account to check your policy status and expiry date. You can also verify your insurance validity through the VAHAN portal by entering your vehicle registration number.

If you purchased your policy through Coverfox, simply sign in to your Coverfox account and download your car insurance policy document.

Your policy number is mentioned on the insurance certificate, policy schedule, premium receipt, and policy confirmation email. If you cannot locate it, contact your insurer with your vehicle registration number and registered mobile number.

Any error in your name, address, vehicle details, engine number, chassis number, nominee, or coverage should be reported to the insurer immediately. The insurer corrects these details by issuing a policy endorsement, which becomes part of your policy document.

The car insurance policy should be transferred to the new owner when you sell your car. Once the ownership transfer is completed at the Regional Transport Office (RTO), the buyer must apply to the insurer to transfer the policy into their name. As per applicable regulations, the third-party insurance cover transfers automatically for a limited period, while the own-damage cover must be formally transferred by the insurer to remain valid.

Yes. A policy can be cancelled by contacting the insurer. If no claim has been made, the insurer refunds the premium after deducting the applicable charges, depending on the cancellation date and policy terms. Once a claim has been paid, the premium is not refundable.

Yes. Every registered vehicle must have its own insurance policy. A single car insurance policy cannot cover multiple cars, even if they are owned by the same individual.

A standard car insurance policy covers the owner-driver's Personal Accident Cover, wherever applicable. Passengers are covered only if an unnamed passenger cover or a similar optional cover has been added to the policy.

The compulsory Personal Accident Cover for the owner-driver is not required if you already hold another valid PA policy of ₹15 lakh covering you as the owner-driver. If you do not have such a cover, it must be included wherever applicable under the prevailing regulatory guidelines.

Damage caused by floods and other natural disasters is covered under a comprehensive policy. However, engine damage resulting from restarting or driving a waterlogged vehicle after water enters the engine is treated as a consequential loss and is not covered unless you have an Engine Protection Add-on.

Damage caused by collisions with animals is covered under a comprehensive policy. Rat-bite damage is covered only if the policy includes a Rat Bite Add-on or if the insurer specifically includes it under the own-damage section. Always check the policy wording.

There is no fixed limit on the number of claims you can make during a policy year. Every claim is assessed independently according to the policy terms. However, repeated claims can result in the loss of your No Claim Bonus and may affect future premiums.

The time depends on the type of claim, document submission, and survey completion. Cashless claims are settled directly with the network garage after approval, while reimbursement claims are processed after all required documents and repair invoices are submitted.

No. Damage that occurred before the policy start date or before renewal is not covered. Insurers only settle claims for losses that occur during the policy period and fall within the scope of the policy.

An own-damage claim results in the loss of your accumulated No Claim Bonus unless you have an NCB Protection Add-on. Losing the NCB increases the own-damage premium at the next renewal.

Several factors influence your renewal premium, including changes in your car's IDV, revised third-party premium rates, add-ons selected, claim history, and the loss of your No Claim Bonus after making an own-damage claim.

Yes. Car insurance premiums attract 18% GST, which is added to the premium payable.

Yes. Many insurers and insurance platforms provide EMI options through partner banks or payment providers. Eligibility, tenure, and interest charges depend on the payment partner.

For older vehicles with a lower market value, the right policy depends on the car's condition and usage. A well-maintained car that is driven regularly can still benefit from comprehensive insurance, while an ageing vehicle with limited usage may only require third-party cover. The decision should balance the premium against the car's current value.

There is no grace period for insurance coverage after your policy expires. Your cover ends immediately on the expiry date. However, you can retain your No Claim Bonus by renewing the policy within 90 days of expiry, subject to the insurer's terms and applicable guidelines.